The streetwear marketplace wars

Headlined by Carlyle's new stake in Supreme and GOAT’s $60M raise, the streetwear market is finally making it into the mainstream. Historically, there’s been very little coverage of this space both on the public and private sides: streetwear and sneakers is a deliberately opaque market, where the community-driven atmosphere must necessarily exclude non-insiders. It’s difficult to analyze without participating.

This is my first yearly attempt at a full scale market analysis: we’re going to look at who the major players are, why I think Grailed is best positioned to win, and how the increasing availability of previously scarce items will impact the landscape. But first: a primer on what streetwear is in the first place.

The Yeezy 350 V2 Blue Tint

(Note: I’m not including Poshmark or Mercari in this analysis, as they don’t deal with much streetwear.)

Streetwear is an aesthetic – or a style of dress – that incorporates unique, scarce, and obscure items into an outfit. The definition is fluid and constantly evolving, but here’s what a typical streetwear outfit might look like.

A typical streetwear outfit (Pinterest)

The streetwear aesthetic relies on pieces, or “grails” as they’re called in the community: outfits are built modularly from sneakers, jeans, shirts, etc. that have their own personality or calling. Here are a few classic streetwear pieces:

Not all items are this expensive, but it typically is a very costly hobby.

Streetwear is heavily community-driven, and this differentiates it from other areas of fashion. One of the major reasons why people invest in streetwear is to connect with others who care about it – walking by someone on the street wearing a similarly obscure outfit often creates a cool level of mutual understanding. The streetwear world thrives on details, limited information, and scarcity (more on that later) – all which lend themselves to small groups and insider culture.

Grailed's in-house blog (Dry Clean Only)

There are entire publications dedicated to streetwear, Twitter accounts that exist solely to give news on when sneakers are for sale, and in-house content operations at the marketplaces we’re going to look at. Staying up to date and understanding trends is more difficult here than in more transparent domains.

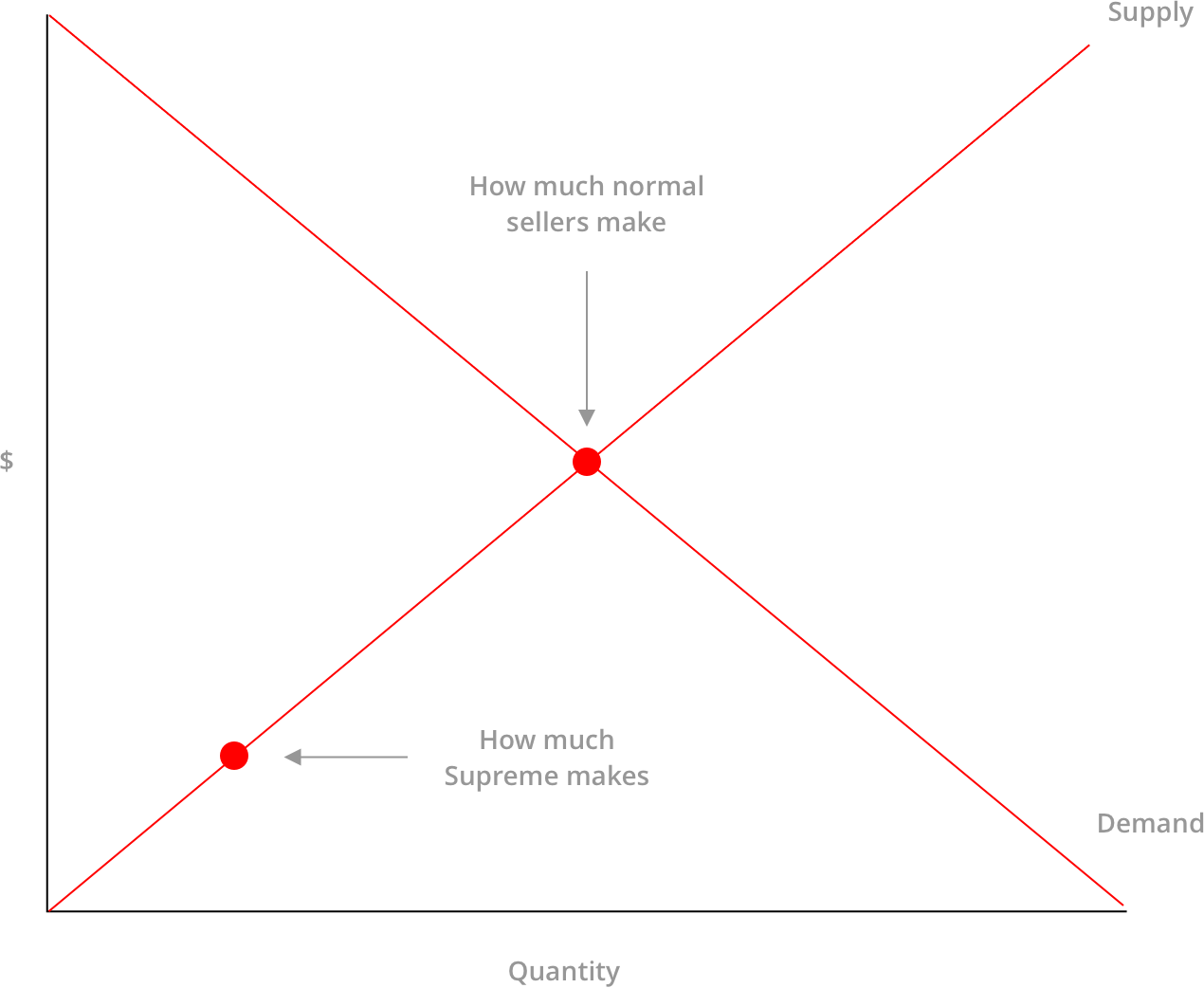

Streetwear is a segment of the fashion market that operates on wartime supply and demand curves. In normal fashion (as with most other lightly regulated markets), manufacturing operates on a supply and demand basis: if clothing sells well, more will be manufactured. Accordingly, there is no aftermarket: what you want will be available at retailers, and you’ll buy it from them.

Figure 1: How streetwear brands play with the supply and demand curves

Streetwear turns that model on its head by fixing supply and ignoring demand. Streetwear relies on a relatively old concept in fashion – manufactured scarcity – to drive hype and create an aftermarket. Essentially, despite the fact that there’s demonstrated demand for a particular item or brand, manufacturers and labels will not increase supply to match it. Pretty weird, right?

It makes a lot of sense if you understand it as a marketing strategy instead of a sales one. By successfully manufacturing scarcity (more on this below), brands can build suspense and future demand. This isn’t a new idea: it exists in luxury brand strategy like at Ferrari, the early days of iPhone, and (remarkably) with Canada Goose sizing. Brands effectively sacrifice meeting current demand with an eye on growing future demand and building a brand.

Manufacturing scarcity isn’t as simple as just not making something. Properly executed scarcity relies on 3 core tenets:

Not all items and releases will follow this playbook (some will be unsuccessful), but brands must execute on each of these to successfully manufacture scarcity. For a great example, let’s take a look at Supreme – the granddaddy of scarcity – and how they’ve built a brand on top of people not being able to buy their stuff.

Supreme is a streetwear brand that makes random stuff: t-shirts, bricks, boxes, a thermos, a hand-axe, and other assorted items. Here’s how it works:

A kayak from Supreme's recent drop (Slashgear)

Attempts at buying this stuff at retail have gotten more and more sophisticated: hackers now sell bots that auto-buy things whenever Supreme releases them. It’s getting a bit nutty.

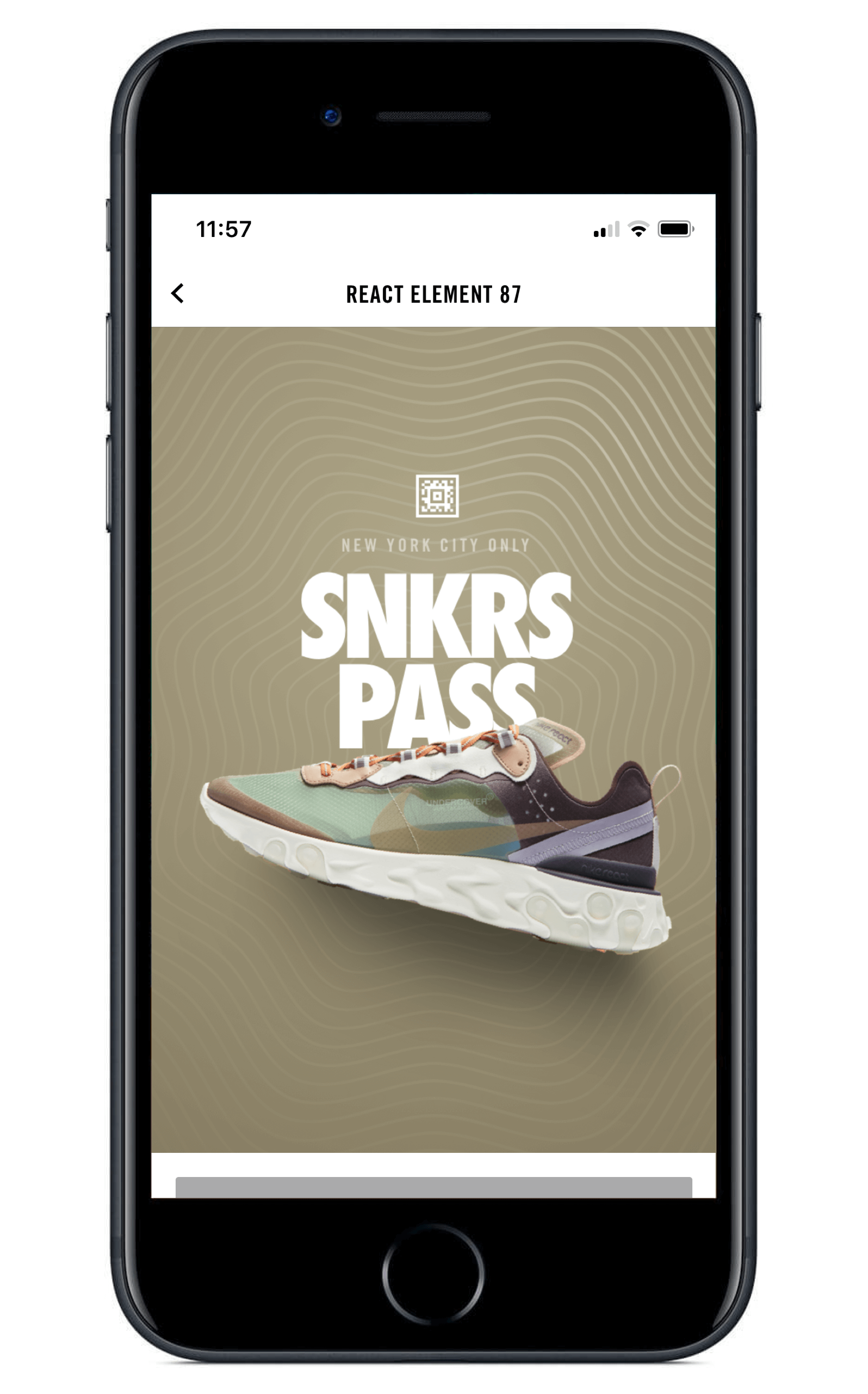

Supreme is its own brand, but bigger apparel manufacturers have also made their stake in this market. Adidas and Nike have both had their share of streetwear success in the past few years (and decades) – Adidas with their Yeezy and Pharrell lines, and Nike with Jordans, SBs, and the recent Virgil Abloh collab. Here’s how these drops work:

A SNKRS App drop

Adidas and Nike have the resources to create their own apps, but not all drops happen this way. Supreme has its own site for drops, and other players make use of physical retail as well. Most Adidas and Nike drops also incorporate their stores as well as resellers.

Drops are a culture in of themselves. The experience of waiting to see if you’ve won a drop is unique, and the line you wait on at the Nike store to pick up your prize is a community. People in the know what you’re there for, and the mutual respect can be intoxicating.

One of the bittersweet parts of “big streetwear” – or when bigger apparel brands have successful streetwear releases – is how they leverage those hits into market share. Unlike indie brands like Supreme that live and die by scarcity, Adidas and Nike are large brands: selling a single line of shoes, even above retail, doesn’t move the bottom line. Instead, they turn their streetwear into normwear. Here’s their playbook:

The Nike React Element 87

Adidas and Nike have done this again and again, and it works. Adidas pioneered their Boost technology with their Yeezy line (a Kanye West collaboration), and it ended up becoming a staple of most of their new models. They also created the Deerupt Runner, which has a very similar silhouette to Yeezys. Nike recently had a bunch of success with their React Element 87: so they copied the sole and upper shape into a mass market shoe that’s half the price.

Market demand creates beautiful art, and then consequently destroys it through mass market copies.

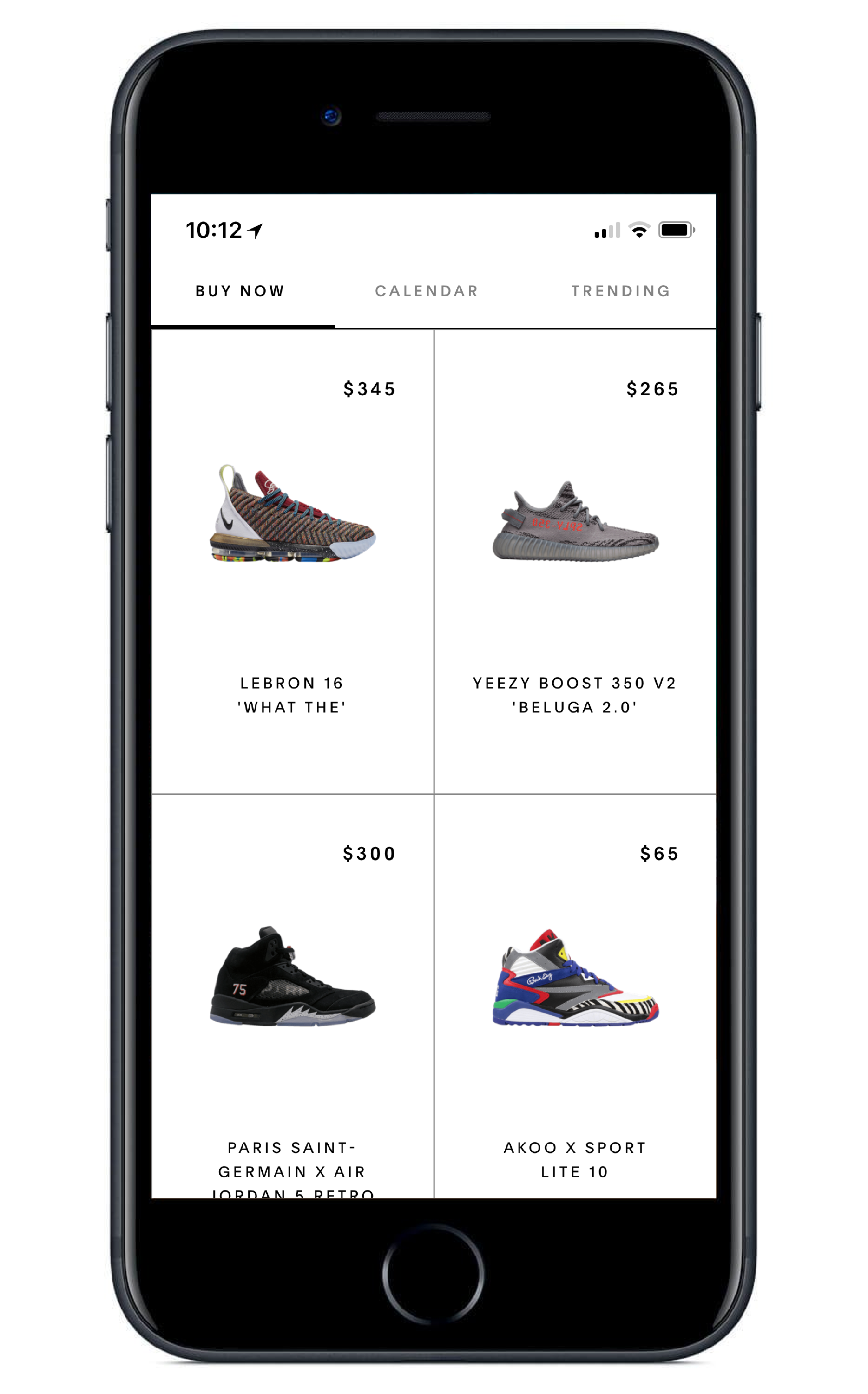

The most important part of the streetwear market is the aftermarket: it’s what really determines how scarce something is and how much respect you’ll garner among the community for owning it. There are 4 major players in the streetwear aftermarket: Grailed, GOAT, StockX, and StadiumGoods. Their platforms allow people to sell their streetwear to the highest bidder, and usually take a commission for bringing supply and demand together.

When evaluating these platforms against one another, there are 4 essential elements that separate the user experience from competitors.

The biggest market inefficiency in streetwear is fraud: whenever things sell for a lot, counterfeit will always be an issue. When buying on an aftermarket platform, you will likely not return if you buy something that turns out to be fake, even if you end up getting your money back. There are three broad methodologies for attacking this problem:

The StockX verified tag

Aftermarket platforms will always take financial responsibility for fraud, but avoiding it is a major part of a good UX.

Streetwear encompasses sneakers, apparel, and accessories: different platforms commit to carrying different things. Sneakers are the most centralized and collectible type of streetwear, so all major platforms support them. Apparel and accessories differ by platform.

There are multiple use cases for streetwear: some buyers want to wear their grails, and some want to collect and/or flip them for a profit. Aftermarket platforms can choose to support selling used items, or commit only to new stuff. New stuff with tags is often called “Deadstock.”

| Verification | Catalog Breadth | Shipping | Condition | |

|---|---|---|---|---|

|

Company | Sneakers | Seller and Buyer | New and Used |

|

Company | Sneakers, limited streetwear, limited accessories | Seller and Buyer | New |

|

Company | Sneakers, limited clothing | Seller and Buyer | New |

|

Community | Sneakers, streetwear, clothing, accessories | Buyer | New and Used |

GOAT is a marketplace just for sneakers, based out of LA and well funded by venture investors. It takes a while to get approved as a seller (it took me 2 months, and was only resolved after I tweeted at them), and all verification goes through their warehouses. They allow sellers to post new, used, and new with defects items.

GOAT has item hierarchy, but still offers used options

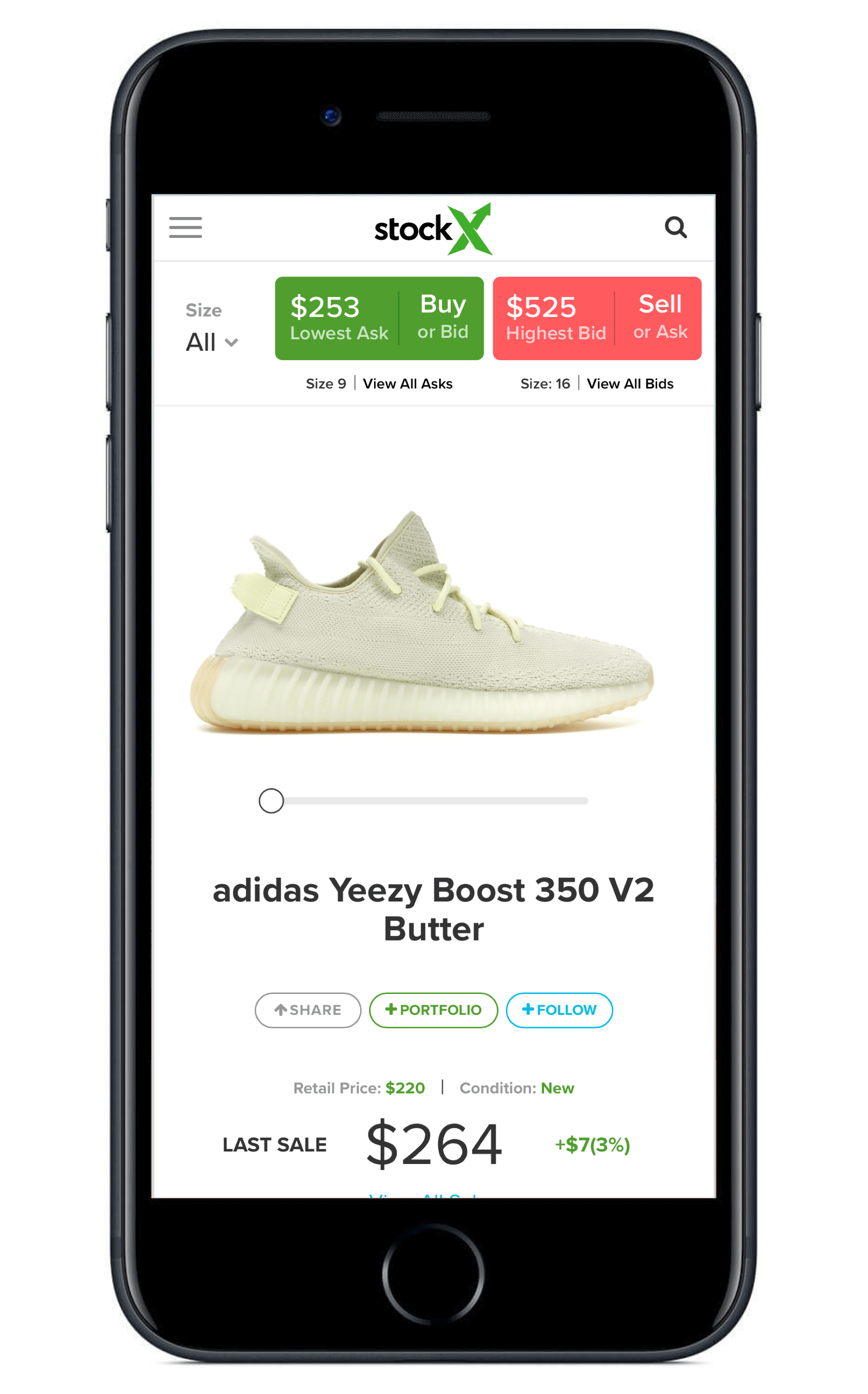

Based out of Detroit, StockX is a marketplace for sneakers and streetwear. The company is big on collecting sales data, and displays some basic analytics for each item (price fluctuations, average price, etc.). They only deal in new items, and just raised a nice round of funding.

StockX abstracts listings into items with bids

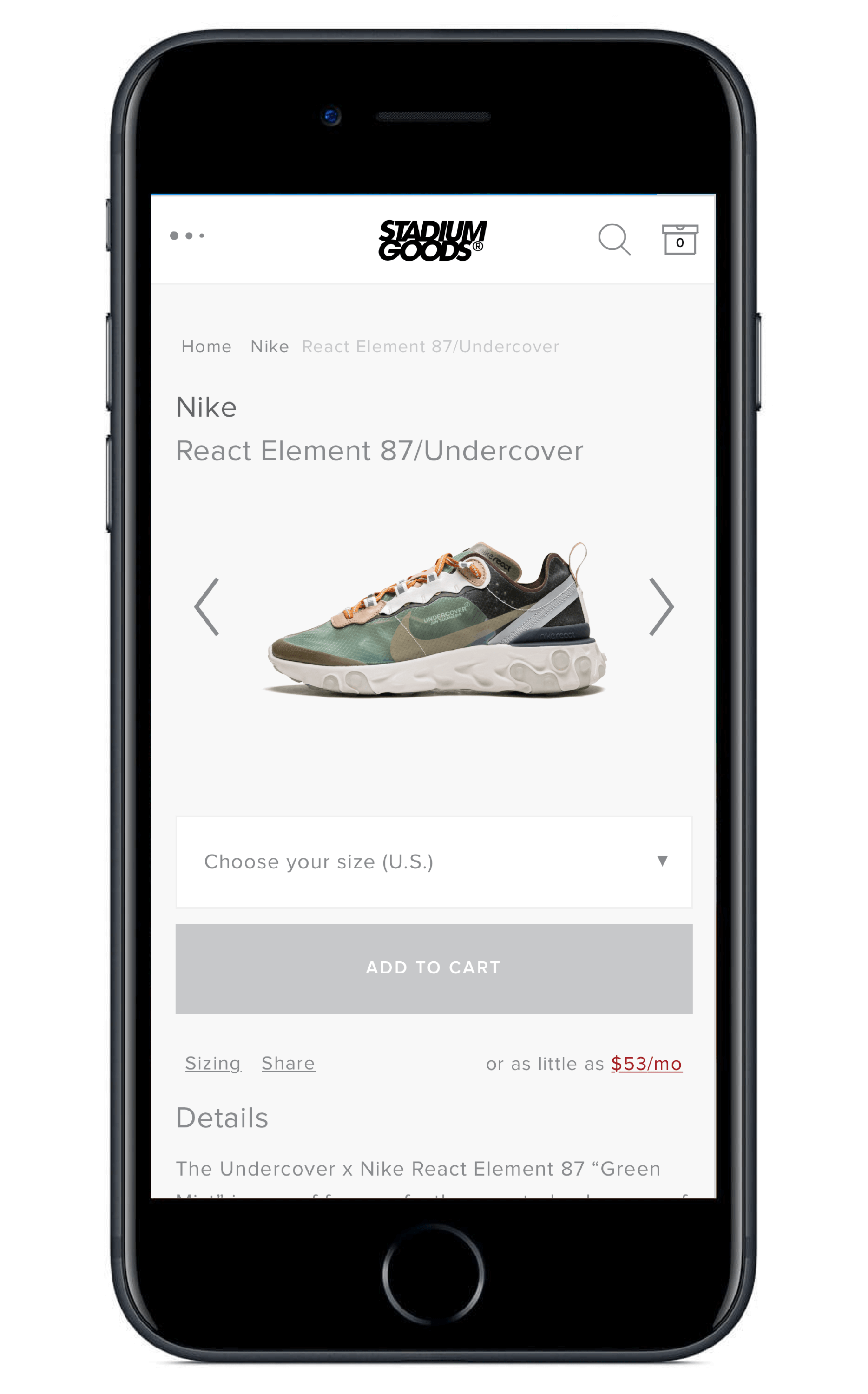

StadiumGoods started out as a physical store, but now has a major presence online. They deal in sneakers and apparel, and raised a seed round from well known investors last year. The site only allows sellers to post new items, and even accepts returns.

StadiumGoods acts like a retail store and abstracts all supply

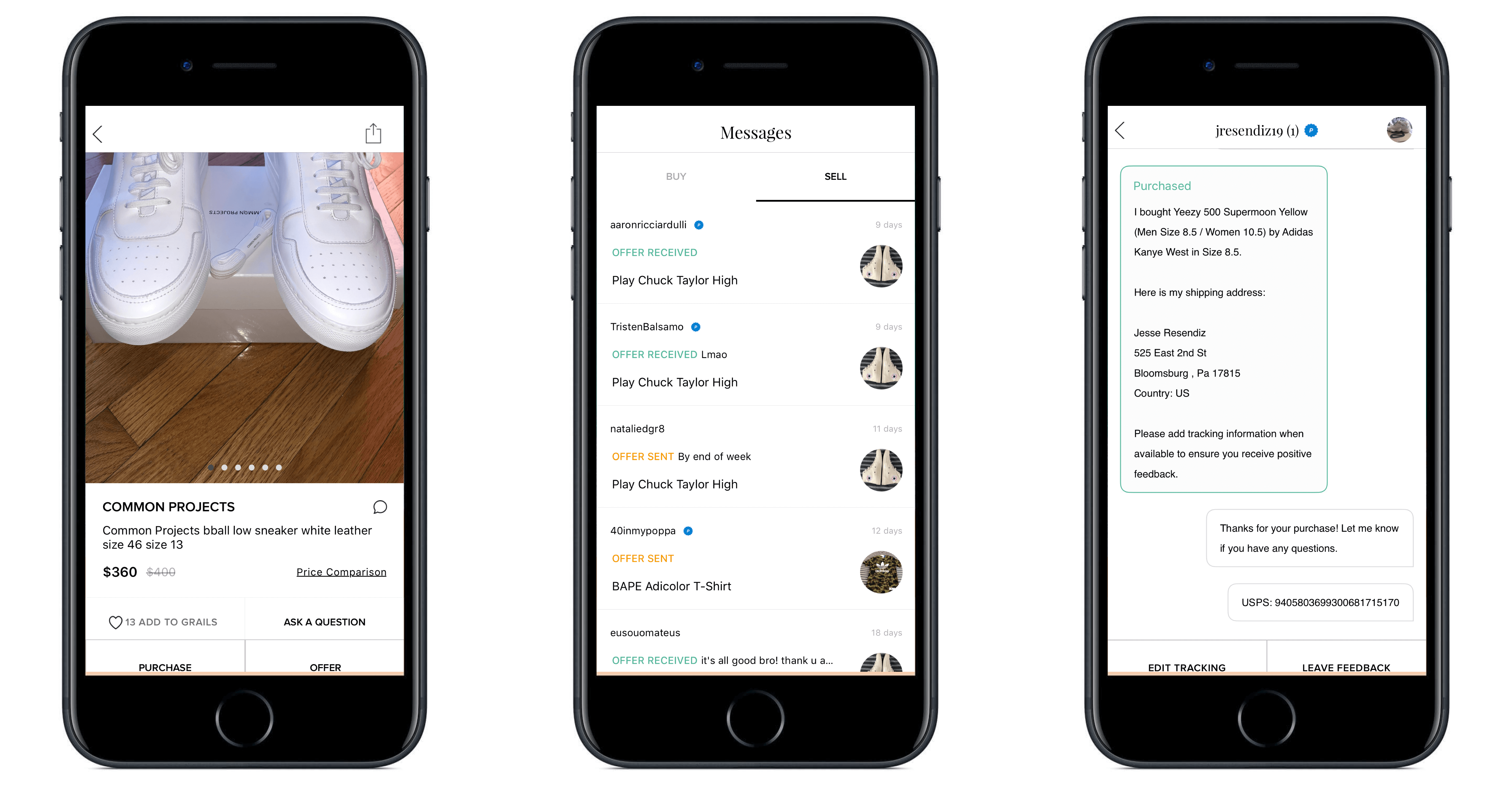

Grailed is a user-driven marketplace where buyers and sellers can exchange anything: from high end streetwear to old Tommy Hilfiger sweatshirts. Unlike the other marketplaces, sellers ship directly to buyers, and verification is community driven. Grailed just raised $15M from awesome investors too.

Grailed listings, messages, and conversations

While all of these platforms are technically marketplaces (they don’t control supply or demand), Grailed is the only true marketplace among them.

Figure 3: Where platforms fit between retail and marketplace

Grailed is very different from the other platforms on this map: it’s a real marketplace:

Items are listed as listings, all individual from each other.

The buying and selling process is iterative and heavy on bargaining.

Verification is community and moderator based.

With all of the money in the market, everybody is asking a few questions:

Let’s tackle these one by one.

The major impetus for newfound investor interest in this area is growth: streetwear has been making its way into the mainstream for years now, and it’s finally reaching critical mass. Supreme is becoming a household name (albeit not a household-owned brand), Kanye is an artistic symbol, and we’ve all heard of kids waiting on lines for Jordans.

Maison Margiela's Paint Splatter GATs

Let’s put some numbers on the board. According to Bain & Co., personal luxury goods sales increased by 5% in 2017 to $309B worldwide. Their report says that 85% of last year’s growth was driven by Generations Y and Z, and “t-shirts, down jackets and sneakers were among the standout categories in 2017, growing by 25%, 15% and 10%, respectively.” There’s not much specificity around what types of streetwear are involved here, since lines can be so blurred and subjective.

That being said, growth of the streetwear market itself is only part of the equation: aftermarket platforms are tapping into a more nuanced segment of the industry. They fill 4 core needs that retailers can’t:

The core insight here is that aftermarket platforms can make money – and indeed do make money – without any new goods being produced. Essentially, with the right strategy, they can create brand new markets by encouraging consumers to buy, sell, and trade with each other. That’s why their success is tied to macro numbers for luxury goods growth, but not limited to it.

Ultimately, for investors, the market question around these platforms is tied both to macro trends (streetwear growth) as well as the ability of these platforms to create their own submarkets.

An important insight in studying complex systems is that some relationships don’t scale, and the same might be true for streetwear. As streetwear grows in popularity, it paradoxically will lose much of the allure that it garners with insiders. Above, we covered the personal and insular element of the streetwear community: part of the fun is that it’s unique, can look kinda weird, and makes other people confused. The more mainstream streetwear becomes, the less those benefits apply.

To understand this trend more deeply, it’s helpful to segment the users of these aftermarket platforms into a few groups:

| "Just Looking" | "Price Scavengers" | "Aspirational" | "Hypebeasts" | |

|---|---|---|---|---|

| Expertise | Low | Low | Medium | High |

| Motivation | Curiosity | Bargain Hunting | Knowledge, opportunity hunting | Find unique items, find good prices |

| Price Sensitivity | Medium | High | High | Medium |

| Substitute Risk | High | Low | Medium | Low |

I suspect that sales on aftermarket platforms are heavily driven by the “Hypebeast” persona: these are people who are experts in streetwear, know exactly what they want, and are extremely savvy on price. As streetwear expands in popularity, this is the group that becomes marginalized and is at risk of leaving / getting into another trend. They also buy the highest price stuff, which translates to higher average revenue for marketplaces (commission based).

For a concrete example of what this means, consider Adidas’s collaboration series with Kanye West: Yeezy. Typically, Yeezys are dropped every few months and are wildly popular: they almost always sell for more than 2x retail on the platforms in question. That has been the case for years, but the landscape has been rapidly changing over the past few months: Yeezys have been becoming more available.

The last two Yeezy drops – the 350v2 Butter and the 500 Utility Black – were dropped in such great quantities that they’re barely selling for more than retail now. Aside from the Yeezy Powerphase (which was generally considered a failure), that’s totally unique in Yeezy history. This is not a fluke: Kanye has publicly expressed his desire to get Yeezys into the hands of whoever wants them, and indicated that the Cream drop on September 21st will be the largest ever.

Yeezy 350 V2 Butter

Yeezy 500 Utility Black

If streetwear staples like Yeezys are readily available for prices similar to retail, what does that mean for aftermarket platforms? Going back to the 4 core benefits of aftermarket platforms:

As streetwear and streetwear culture becomes more mainstream, it begins to erode the value proposition of aftermarket platforms for certain user personas. Growth will mean moving

From

lower volume, higher priced insider items

To

higher volume, lower priced mainstream items

If the bulk of aftermarket platforms rely on the “Hypebeast” persona to drive high priced sales on their platforms, this market shift means that the end of that is near, and these platforms are starting to hit the mass market. I suspect that’s the basis of many of these large funding rounds.

The aftermarket platforms in this market all started out by catering to a niche group – “Hypebeasts” – that were reliable, serviceable, and great pilot customers. But hitting venture scale means moving on to service other market segments. Non-core users – in our case users that aren’t heavily committed to streetwear – have a different set of priorities:

| Previous Core Customers | New Customers | |

|---|---|---|

| Price Sensitivity | Low-Medium | High |

| UX Focus | Low | High |

| Fraud Tolerance | High | Low |

| Platform Loyalty | High | Low |

Platforms that can take advantage of this shift will have a much larger market to cater to, but the shift will be difficult to execute. Post-shift, they’ll also need to worry about much stiffer competition with traditional retailers and e-commerce players. New customers will expect fast shipping, clear pictures and expectations of what they’re getting, and will have no tolerance for fraud: this is a different persona, or in other words “what got you here won’t get you there.”

| Pre-scale Platform | Post-scale Platform | |

|---|---|---|

| Catalog | Narrow, high value | Wide, multi-value |

| UX | Segmented | Seamless: fast shipping, strong customer service |

| Community | Content, raffles | Arguably not important |

| Competition | Sample sales, drops, high-end retailers | Wide variety of retailers |

As with many niche businesses, scaling will mean a much larger market opportunity but consequently a higher risk, less differentiated business. They’re shifting from a true marketplace to more of a quasi-retailer. I would be surprised if a few of these platforms don’t start to work with brands directly for listings.

The major impetus for newfound investor interest in this area is growth: streetwear has been making its way into the mainstream for years now, and it’s finally reaching critical mass. Supreme is becoming a household name (albeit not a household-owned brand), Kanye is an artistic symbol, and we’ve all heard of kids waiting on lines for Jordans.

Figure 7: StockX has the best seller UX among the group

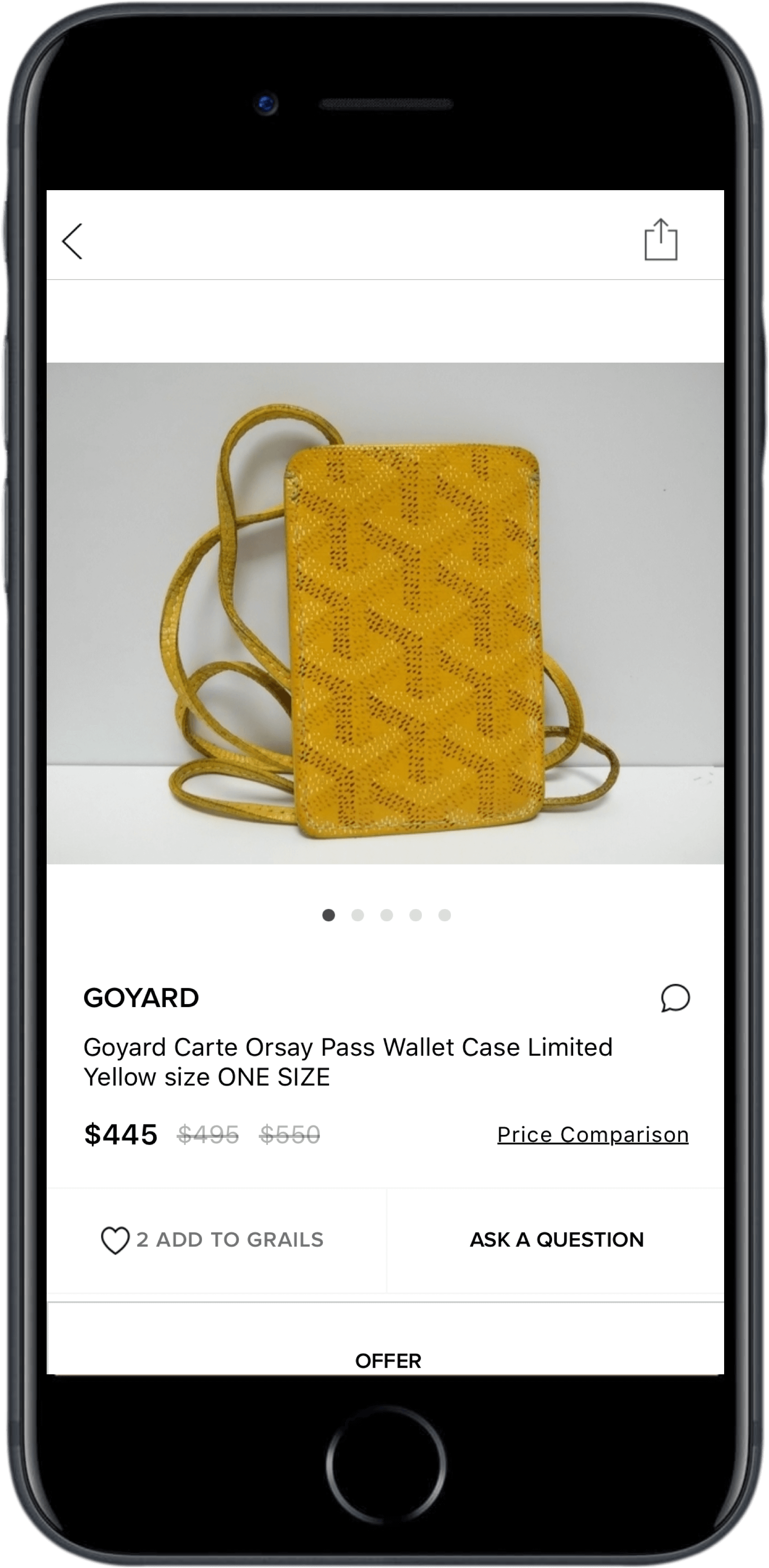

StockX has the best seller UX in the group. There’s no seller verification process required (unlike GOAT), you don’t need to upload any pictures (like Grailed), and the product makes the process fairly simple and clear. GOAT has a relatively simple process, buy you need to get verified first: that process is totally opaque and disappointingly unprofessional for a company of their stage. Grailed is totally self serve: selling is an iterative process of lowering your ask and conversing with buyers (more on that later).

Figure 8: Grailed has the most clunky buyer UX, and GOAT and StockX are tied for the best

Buying on GOAT and StockX is ridiculously easy: find your size, pay, and be done with it. Shipping is too slow because of the required verification at their warehouse, but that should improve over time. StadiumGoods prices tend to be much higher for buyers, which hurts the UX. And buying on Grailed relies heavily on user knowledge and understanding, which isn’t great at scale when your users are novices.

Figure 9: Grailed has the greatest catalog breadth of the bunch

Grailed is miles ahead of the competition in catalog breadth: you can pretty much find anything on there. That’s because they don’t require verification, and sellers ship to buyers directly. StockX has a very good selection of sneakers, streetwear, and accessories. GOAT only sells sneakers, and StadiumGoods is limited even though they’re broad in categories.

Figure 10: Grailed has by far the most functionality app-wise in the group

Grailed takes the trophy again here: with messaging, advanced filters, and an impressive content operation, it’s a much richer platform than the others. GOAT’s capabilities around used and new with defects items puts it ahead of StockX and Stadium Goods, which basically are just e-commerce platforms (although StockX does have a newsletter).

Overall, I don’t see any of these platforms as best positioned right now. StockX and Stadium Goods are ideal for buyers who know exactly what they want and don’t want to bargain. Grailed is much more of a community, and is a place to buy tons of different things with the flexibility to negotiate on price. GOAT finds a sort of middle ground.

Aftermarket platforms effectively have two options to weather the incoming storm that is streetwear ubiquity:

The platforms we’re looking at split across these approaches.

GOAT, StockX, and Stadium Goods seem to be focused on the former: creating a more retail-like experience within an actual marketplace. They seek to effectively commoditize supply and abstract it to “just sneakers” or “just clothing” – regardless of where it came from. Grailed, on the other hand, seems to be taking another approach: and I think they’re positioning themselves best.

As a retail-like player, there’s one giant problem that these companies will face: validation and fraud measures don’t scale. As the process currently stands, here’s how it works (for GOAT, StockX, and StadiumGoods):

This (tedious) process avoids fraud, but is a major setback for both buyer UX (shipping necessarily takes a long time) and profitability. As their volume grows, these companies need to keep hiring employees to verify merchandise. Ultimately, these platforms will need to find a way to shorten shipping time, improve the verification process, or hope that a superior UX will outweigh the downsides of manual verification.

Grailed, on the other hand, has sellers ship directly to buyers and relies on communities and moderators for verification. We can assume that they have higher fraud rates, but their overhead as a company is much lower. This process is much more scalable in theory.

But the major difference between Grailed and the other platforms we’ve covered – and the reason why I think they’re best positioned to be successful – is that they haven’t started making the shift towards providing a more retail-like experience. Buying and selling on Grailed is still a highly manual, iterative, bargaining-heavy process. It’s clear that they’re doubling down on being the place for (a) community, and (b) used stuff.

Grailed selling is iterative (note the transparent price changes)

I have no doubt that GOAT, StockX, and StadiumGoods can grow into large retailers: the question is only what their margins will look like, and whether that’s really a business that they want to be in. Grailed seems to be positioning itself to stick firmly in the marketplace arena and building features around making that better. They’ve shown no initiative towards commoditizing supply.

The question for Grailed is complex: can they improve the UX of both buying and selling without compromising their insider status, marketplace feel, and dominance in used stuff? Here are few features that might help them do that (surprise: many are Machine Learning based):

If Grailed can execute on some of these new features, they’ll move closer towards being an independent marketplace with a great UX for both buyers and sellers: and that’s what ultimately will win this market. In summary, here’s why I think Grailed is strongly positioned:

That being said, the impacts of streetwear becoming mainstream are fairly unpredictable. I’ve attempted to explain what I think it means for the market, but it’s anyone’s guess.